Ad

Ad

Progress for group 0 ad

Omer Hussein

Addis Ababa, Ethiopia

In the past few months, Ethiopia’s financial landscape has been witnessing a significant shift with the introduction of new banking fees and an increase in previous fees by the leading bank in Ethiopia, the Commercial Bank of Ethiopia (CBE). This move has sparked debates among the populace, raising questions about its necessity and fairness. As the banking sector navigates through these changes, it is imperative to dissect the rationale behind the introduction of these fees and evaluate whether they are indeed justified.

In October 2023, the Commercial Bank of Ethiopia announced its new service tariffs. A set of recent charges were introduced including

The fees were initially higher than this, however, the public uproar that followed led to the bank to respond to this lower set of service charges.

This new service charge package from the bank with the leading market share in Ethiopia, will surely encourage other banks to follow suit.

This trend in the banking industry has not only introduced new fees but also increased existing service charges. A glaring example is the bank’s ATM transaction fees. CBE’s transaction fees increased by 75%, from 0.2% to 0.35%.

While no official statement has been provided by the bank regarding the reason behind the new service charge fees, it’s speculated that the NBE’s decision in August 2023, capping yearly credit expansion at 14% in an effort to reduce inflation, is playing a major role.

While it is true that the income generated from interest constitutes around 3/4th of the bank’s total income in the past three years, the 14% yearly credit expansion cap will make no tangible difference in its income generated from interest. This is evidenced by the fact that in the past three years, the yearly credit expansion growth of CBE was 22.6%, 10.1%, and 14.7%, respectively.

In my opinion, they are not. I have three reasons to think why.

Firstly, the service charges enclosed above were not actively advertised to the public. The National Bank of Ethiopia’s consumer protection directive issued in 2020 aims to regulate all financial service providers and promote financial inclusion, trust, and confidence in the financial system while maintaining stability. Article 5.1.2, clearly states that financial service providers shall not charge a financial customer any fee that was not previously disclosed.

Secondly, banks who are typically profitability powerhouses should not be able to further extract more income from the average citizen. CBE’s recorded profits after tax in the past fiscal year were around 17.4 billion birr. A temporary cap from the NBE that would at most result in a slight reduction in profit should not translate to such a high burden on the customers.

Lastly, we always hear about digitalization and inclusion in the financial sector. Making people pay such excessive amounts for using digital financial services would surely drive people away from utilizing mobile banking and DFS, and this would lead to financial exclusion, an outcome no stakeholder in the industry desires.

Efforts to preserve profit margins, coupled with the recognition that approximately 95% of Ethiopian bank clients maintain savings of less than 100,000 birr, should prompt the bank to explore alternative strategies to address the NBE credit expansion cap.

I propose that they consider raising the minimum thresholds for free transactions (withdrawals or transfers) to at least 20,000 birr. To compensate for potential revenue loss, they could impose higher transaction fees on accounts with substantial savings balances. While a fee of 5 or 10 birr may hold significant value for individuals below the poverty line, a fee ten times that amount could be inconsequential for business accounts engaged in transactions totaling six, seven, and higher figures in birr.

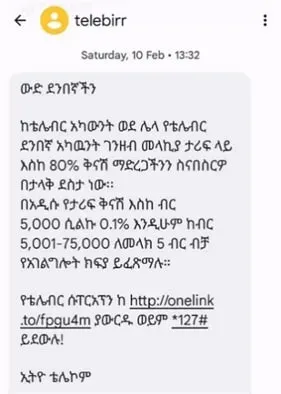

Ethio Telecom with its mobile money platform telebirr, seems to have gotten wind of the public’s offense to the bank’s increased service fees.

In an effort to attract more customers, telebirr has announced a major price cut (80% off) on the person-to-person (P2P) transfer tariff. The tariff is now just 0.1% for transfers up to 5,000 birr (from 0.5% previously) and a flat 5 birr for transfers from 5,001 up to 75,000 birr.

Chasing short-term profits by introducing high service charge fees will cost the bank eventually. Mobile money operators, foreign banks, and local banks who have yet to introduce such service charges will attract more customers, gain a higher market share, and enjoy a more stable and profitable future in the long term.

____________

Omer Hussein, an Associate at Shega Insights, has a keen interest in exploring Ethiopian issues through the eyes of the common citizen. He can be reached at [email protected].

Share this post:

Omer Hussein

At Shega, we do more than tell stories. We help you make an impact. Our platforms, data, and expertise connect brands, organizations, and investors to the audiences and insights that matter.

Reach, engage, and grow with us.

Get in TouchLatest Stories

22 December 2025

𝗗𝗲𝘀𝗶𝗴𝗻𝗲𝗱 𝗳𝗼𝗿 𝗪𝗵𝗼𝗺? 𝗧𝗵𝗲 𝗠𝗶𝗿𝗮𝗴𝗲 𝗼𝗳 𝗪𝗼𝗺𝗲𝗻-𝗖𝗲𝗻𝘁𝗿𝗶𝗰 𝗗𝗶𝗴𝗶𝘁𝗮𝗹 𝗙𝗶𝗻𝗮𝗻𝗰𝗲 𝗶𝗻 𝗘𝘁𝗵𝗶𝗼𝗽𝗶𝗮 QA

By Chilen14 December 2025

From Campus Idea to Satellite TV: Ethiopia Gets Its First Home Shopping Channel QA test

By ChilenLatest Stories

𝗗𝗲𝘀𝗶𝗴𝗻𝗲𝗱 𝗳𝗼𝗿 𝗪𝗵𝗼𝗺? 𝗧𝗵𝗲 𝗠𝗶𝗿𝗮𝗴𝗲 𝗼𝗳 𝗪𝗼𝗺𝗲𝗻-𝗖𝗲𝗻𝘁𝗿𝗶𝗰 𝗗𝗶𝗴𝗶𝘁𝗮𝗹 𝗙𝗶𝗻𝗮𝗻𝗰𝗲 𝗶𝗻 𝗘𝘁𝗵𝗶𝗼𝗽𝗶𝗮 QA

22 December 2025

From Campus Idea to Satellite TV: Ethiopia Gets Its First Home Shopping Channel QA test

14 December 2025

𝗗𝗮𝘁𝗮 𝗦𝗼𝘃𝗲𝗿𝗲𝗶𝗴𝗻𝘁𝘆, 𝗧𝗲𝗰𝗵-𝗦𝗮𝘃𝘃𝘆 𝗖𝗶𝘃𝗶𝗹 𝗦𝗲𝗿𝘃𝗮𝗻𝘁𝘀 & 𝟭 𝗺𝗶𝗹𝗹𝗶𝗼𝗻 𝗜𝗧 𝗷𝗼𝗯𝘀: 𝗨𝗻𝗽𝗮𝗰𝗸𝗶𝗻𝗴 𝗘𝘁𝗵𝗶𝗼𝗽𝗶𝗮’𝘀 𝟮𝟬𝟯𝟬 𝗗𝗶𝗴𝗶𝘁𝗮𝗹 𝗥𝗼𝗮𝗱𝗺𝗮𝗽 on Qa strapi

11 December 2025