Ad

Ad

Progress for group 0 ad

Anteneh

Addis Ababa, Ethiopia

While Ethiopia draws lessons from the financial inclusion successes of its neighbors, we need to ask bigger questions. How should we tailor financial solutions to truly resonate with the unique socio-economic fabric of Ethiopia?

Catch up with the first of many monthly analysis articles by AKOFADA (Advancing Knowledge on Financial Accessibility and DFS Adoption), a project that is working to increase the knowledge base of Ethiopia’s DFS ecosystem.

_________

In 2016, I found myself along with my five Ethiopian teammates, stuck on a road leading from Entebbe International Airport, on the shores of Lake Victoria, to Kampala, the capital of Uganda.

The reason? We were attending a regional youth leadership conference. This trip marked my first visit to another African country, and my curiosity was piqued. Amidst the traffic congestion, a few things became evident.

The roads appeared much narrower than those I was accustomed to back home. Motorbikes, locally known as Boda Boda, swarmed the streets, outnumbering four-wheelers—an unusual sight for someone from Ethiopia.

Fast forward to August 2018, and I am in Nairobi, Kenya, walking down the road from my temporary apartment to Africa’s Talking Kenya office, a short five-minute journey. Tasked with helping Africa’s Talking, a communication and payment solution provider, launch and grow in Ethiopia, my mission in Nairobi was to understand how things operated at the company’s headquarters.

Much like my experience in Uganda, the roads in Nairobi felt narrower and predominantly one-way, with motorcycles being common in sight.

In contrast to Uganda and Kenya, Addis Ababa and much of Ethiopia rely less on motorcycles and narrow streets and more on wider roads and cars. This difference in transportation modes can be partly attributed to Ethiopia’s unique historical and socio-political context.

However, my most significant learning came from observing and interacting with professionals and residents in Nairobi. Many owned or had inherited land outside the city, maintaining ancestral connections or a rural base despite their urban lifestyles. This reflection of the deep-seated value of preserving familial and rural ties amidst urbanization struck me. It prompted me to consider if a similar sentiment exists among Addis Ababa’s urbanites, inviting contemplation on the cultural nuances shaping behaviors and choices in urban Ethiopia, including financial service.

This journey through the roads of Uganda and Kenya, along with my experiences in Ethiopia, underscores a critical point: no two countries are the same, even in Africa and East Africa.

The above two East African countries I visited in the past surely have similar things. First, they both made significant strides in financial inclusion over the past decade. Particularly, Kenya is viewed as a model for achieving financial inclusion through mobile technology, showcasing a leapfrogging success story.

In contrast, Ethiopia embarked on this path somewhat later. But the country is now full of action, with numerous activities supporting and enhancing the financial ecosystem.

These efforts, driven by both service providers and facilitators, signal a growing recognition of the critical role of financial inclusion in countries’ journeys of transformation. As Ethiopia treads this path, it draws inspiration from its neighbors’ successes.

However, these efforts often seem to operate without full recognition of the distinct paths countries go through, tending towards a strategy of imitation from models like Kenya’s rather than tailoring unique solutions that reflect Ethiopia’s unique socio-economic landscape.

Drawing on this notion, we can set the stage for a deeper dive into the critical question of how we should look at and assess Ethiopia’s quest to bring financial services to the majority.

Before we delve into details, let’s first establish a foundation and conduct a reality check. Financial inclusion is a word that gets thrown around a lot these days. It encompasses ensuring that all individuals and businesses, regardless of their standing, have access to basic and affordable financial services, such as payments, credit, savings, and insurance, which are fundamental to participating fully in the economy.

The concept of financial inclusion has emerged as a cornerstone for economic and social development. But there are also those who argue that economic development is a prerequisite for financial inclusion.

The academic world provides two theoretical frameworks to describe the relationship between financial development (including financial inclusion) and economic growth: the demand-driven hypothesis and the supply-leading hypothesis.

The supply-leading hypothesis posits that providing financial services spurs economic growth by equipping individuals and businesses with the resources needed for investment and expansion, effectively acting as a catalyst for economic activities. On the other hand, the demand-driven hypothesis suggests that economic growth creates a need for financial services, with the development of the financial sector being a response to increased economic activities and the rising financial needs of a growing economy.

A study by Tekilu Tadesse and Jemal Abafia, ‘The causality between Financial Development and Economic Growth in Ethiopia,’ using data from 1975–2016, supports the ‘supply-leading’ hypothesis, showing that financial development positively impacts Ethiopia’s economic growth both in the short and long term, highlighting the critical role of financial sector advancements in driving economic progress.

Many initiatives aimed at promoting financial inclusion in Ethiopia, whether spearheaded by governmental bodies or international development organizations, appear to be predicated on the principles of the supply-leading hypothesis.

In reality, the relationship between financial inclusion (and, more broadly, financial development) and economic growth is complex and can involve elements of both hypotheses. Effective strategy-making often seeks to leverage the interplay between supply and demand, recognizing that:

While acknowledging the interplay, let’s look at where we are. Ethiopia stands at a critical juncture in its journey towards comprehensive financial inclusion. Despite considerable strides in recent years, propelled by policy reforms and consolidated efforts, the Ethiopian financial ecosystem faces unique challenges and opportunities in its quest to provide universal access to financial services.

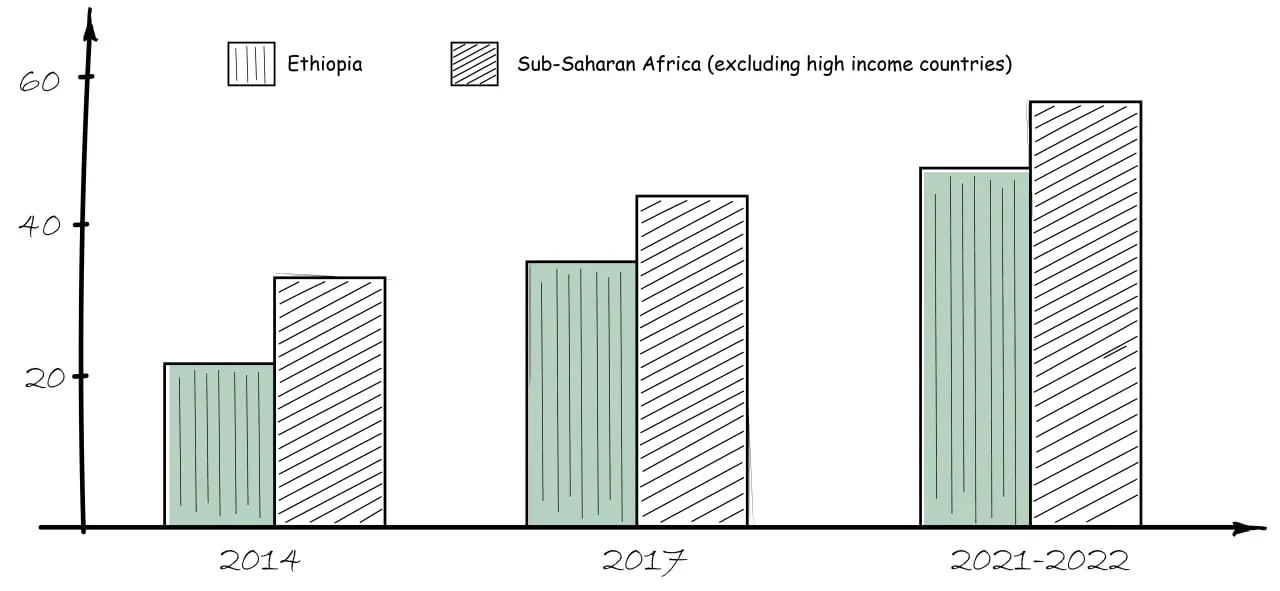

Recognizing the importance of having a consolidated approach towards financial inclusion, Ethiopia put forward the first National Financial Inclusion Strategy (2014–2020), followed by an updated strategy covering 2021–2025. The National Bank of Ethiopia is focused on achieving a significant milestone: ensuring that 70% of adults have bank accounts by 2025. One of the pillars of recently introduced Ethiopia’s National Bank New Strategic Plan 2023–2026 policy is also ensuring financial inclusion, deepening, and digitization.

Share this post:

Anteneh

At Shega, we do more than tell stories. We help you make an impact. Our platforms, data, and expertise connect brands, organizations, and investors to the audiences and insights that matter.

Reach, engage, and grow with us.

Get in Touch

Healthcare Startup Debuts Prescription Platform

03 March 2025

Billionaire’s Son Fumbles Bag with Fintech Startup

24 November 2024

Latest Stories

22 December 2025

𝗗𝗲𝘀𝗶𝗴𝗻𝗲𝗱 𝗳𝗼𝗿 𝗪𝗵𝗼𝗺? 𝗧𝗵𝗲 𝗠𝗶𝗿𝗮𝗴𝗲 𝗼𝗳 𝗪𝗼𝗺𝗲𝗻-𝗖𝗲𝗻𝘁𝗿𝗶𝗰 𝗗𝗶𝗴𝗶𝘁𝗮𝗹 𝗙𝗶𝗻𝗮𝗻𝗰𝗲 𝗶𝗻 𝗘𝘁𝗵𝗶𝗼𝗽𝗶𝗮 QA

By Chilen14 December 2025

From Campus Idea to Satellite TV: Ethiopia Gets Its First Home Shopping Channel QA test

By ChilenLatest Stories

𝗗𝗲𝘀𝗶𝗴𝗻𝗲𝗱 𝗳𝗼𝗿 𝗪𝗵𝗼𝗺? 𝗧𝗵𝗲 𝗠𝗶𝗿𝗮𝗴𝗲 𝗼𝗳 𝗪𝗼𝗺𝗲𝗻-𝗖𝗲𝗻𝘁𝗿𝗶𝗰 𝗗𝗶𝗴𝗶𝘁𝗮𝗹 𝗙𝗶𝗻𝗮𝗻𝗰𝗲 𝗶𝗻 𝗘𝘁𝗵𝗶𝗼𝗽𝗶𝗮 QA

22 December 2025

From Campus Idea to Satellite TV: Ethiopia Gets Its First Home Shopping Channel QA test

14 December 2025

𝗗𝗮𝘁𝗮 𝗦𝗼𝘃𝗲𝗿𝗲𝗶𝗴𝗻𝘁𝘆, 𝗧𝗲𝗰𝗵-𝗦𝗮𝘃𝘃𝘆 𝗖𝗶𝘃𝗶𝗹 𝗦𝗲𝗿𝘃𝗮𝗻𝘁𝘀 & 𝟭 𝗺𝗶𝗹𝗹𝗶𝗼𝗻 𝗜𝗧 𝗷𝗼𝗯𝘀: 𝗨𝗻𝗽𝗮𝗰𝗸𝗶𝗻𝗴 𝗘𝘁𝗵𝗶𝗼𝗽𝗶𝗮’𝘀 𝟮𝟬𝟯𝟬 𝗗𝗶𝗴𝗶𝘁𝗮𝗹 𝗥𝗼𝗮𝗱𝗺𝗮𝗽 on Qa strapi

11 December 2025

Healthcare Startup Debuts Prescription Platform

03 March 2025

Billionaire’s Son Fumbles Bag with Fintech Startup

24 November 2024